Liquidity in banks is like water in a big city; people assume that when they turn on the tap it is there. The banking world is now a year away from a major change in how it has to measure its intraday liquidity usage. How it responds matters, to the tune of millions in expense, up or down. Every billion dollars of liquidity costs at least £10 million per year. How banks approach this is far more important than any other cost saving exercise. No amount of other cost cutting can readily make up for these costs if they are incurred. IN terms of heads, that is between 66 and 200 of them. This matters.

Most city dwellers spare scarcely a thought for exactly how the water made it there and little, and have little, if any, awareness of the cost and almost total ignorance of the fact that most of the pipes and plumbing is old, leaky & inefficient. In banks, the equivalent is that most staff assume that cash will be in the right place at the right time; they know the firm has a series of Nostros and Depots and has a team called “Cash management”, but have little insight into what those people do. If you looked after the day-to-day operations of a water company your job would be to make sure there is enough water in the right place at the right time. Somebody else has built the pipes and the reservoirs.

Most city dwellers spare scarcely a thought for exactly how the water made it there and little, and have little, if any, awareness of the cost and almost total ignorance of the fact that most of the pipes and plumbing is old, leaky & inefficient. In banks, the equivalent is that most staff assume that cash will be in the right place at the right time; they know the firm has a series of Nostros and Depots and has a team called “Cash management”, but have little insight into what those people do. If you looked after the day-to-day operations of a water company your job would be to make sure there is enough water in the right place at the right time. Somebody else has built the pipes and the reservoirs.

In a bank, the equivalent of the production team is Cash Management. Their job is to have the right amount of money in the right place at the right time. Understandably, there are some rules associated with that function, requiring the banks to have reserves, in the form of the “Liquidity Buffer”, to ensure they can meet their obligations. In the current wave of regulation being imposed on banks, there is a new directive aimed at ensuring the banks can precisely measure their intraday liquidity positions. Not a totally new requirement, but one that is now very precise.

The new directive comes from the BCBS, the Basel Committee for Banking Supervision (for more detail click here). This directive sets out seven measures that banks will required to make of credit taken and credit given. Over the coming weeks, this Blog will go into the details of what the measures are and how the banks might address them. We will start though with why this is important and how the banks risked having truly massive extra new costs imposed on them.

The “Liquidity Buffer” is the pot of reserves that banks are obliged to keep in place to ensure they can meet liabilities in terms of stress. The idea is that the banks have so called High Quality Liquid Assets (“HQLA”) that they can use to finance outgoings in a crisis. Typically a large bank will have a buffer in excess of $100 billion, with perhaps $15 billion allocated to intra-day needs. At a simple level, the new requirements are going to allow for more accurate view of what that intraday liquidity buffer should be. So the banks have to measure. What might happen? One large European IB has already been through this test; they struggled to measure exactly, but managed to do some of it. The result was that their requirement went up from $9 billion to $15 billion in one instant jump. Between $60 and $90 million in extra expense at a swoop. “Between” because the cost of funding varies between 100 and 150 basis points. Now, what this shows is that if you can measure, there is a good chance the regulator pushes the requirement up by a meaningful, large amount, so it follows that if you cannot properly measure, then the number goes up even more.

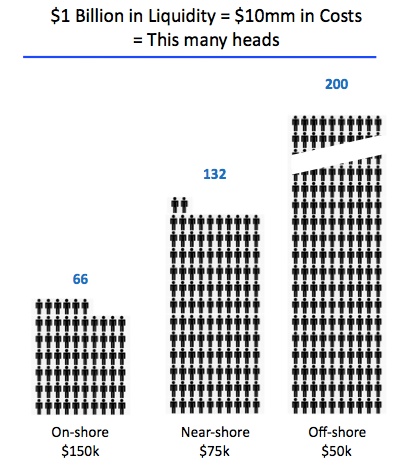

Over the next weeks, I will look at the exact requirements and now one might take action. This week, I would like to sign-off with “lesson to be learned”. If the liquidity requirement moves by 1B, that is at least $10 million worth of expense or saving. Put that in perspective in terms of headcount, which is normally the thing banks chop to save cost. The infographic shows what $10mm means in people terms.

Lessons Learned: Banks will have to measure. That is certain. Ideally, they will be ready to optimise that number and improve their processes. If they do not grasp the nettle, it is hard to see how any other headcount chopping will help them on the cost front.

A personal request: The book of the Blog is in the works. Your support would be appreciated on two fronts:

- Please subscribe, if you don’t already.

- Please share this with a friend or two and ask them to subscribe too.

If the comments are wide of the mark and not offering anything of use, please comment or make contact directly via E-Mail.

Share on: