A recent Bloomberg article has caused a ripple or two. Two big name items have collided to cause this effect: the Blockchain and the involvement of industry maven, Blythe Masters, who as a young hot shot at JP Morgan invented the CDS product. The article is a must read and with it, the following pinch of salt, or rather the awareness that one vital ingredient is missing.

In previous posts, I have highlighted the potential that the Blockchain offers. That vision of the huge potential is one shared by the very astute Ms. Masters and her partners, as well as other luminaries such as Reid Hoffman. Blockchain is not to be confused with or mixed up with Bitcoin; the former is a very valuable tool to enable transaction processing, the latter is a mooted ersatz for real money in the form of fiat currencies, i.e. ones issued by central banks.

The missing ingredient is simple, but elusive: money. Bitcoin is simply too untrustworthy (see prior post). There is also no obvious 100%. substitute. The marketing tsunami that is Ripple would have us believe that the solution is at hand. Understanding where change is needed in matters of money makes it essential to understand the limitations of the current market infrastructure, which set out some laws of physics which even Silicon Valley smarts cannot compensate for.

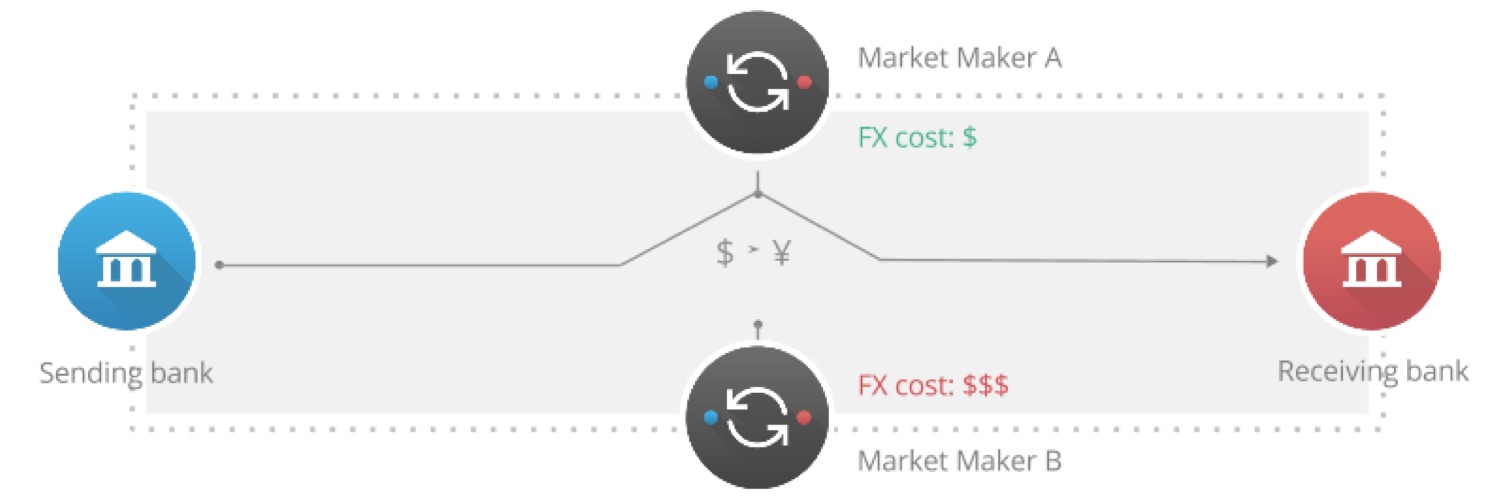

The graphic is Ripple’s own view of how it enables an international payment via the FX markets. The premise is that the market makers have liquidity and magically make everything happen instantly. Let’s use a real example to see how this might work. I live in Switzerland and regularly need British Pounds, GBP. Assume I want to send GBP 1’000 from my Swiss account to my UK one. According to the Ripple model, or at least my understanding of it, my Swiss bank, Credit Suisse (CS), will use the Ripple platform to find a counterpart who has GBP liquidity and will then send on GBP to my UK bank, RBS. For the sake of illustration, let’s assume that Lloyds Bank plays this role.

Source: Ripple

All this with the promise of instant payment. Whilst this would be great for me as a customer, my happiness is only given if the banks involved will accept the laws of physics as they apply to payments:

First, CS and Lloyds need to exchange Swiss Francs for Pounds. there is currently no means to do that instantly with any finality. It could be done for value the next day via an industry utility, CLS, but not instantly. The two banks could agree to hold accounts with each other; CS could credit Swiss Francs to an account in Lloyds’ name and vice versa. But, that involves credit risk with each bank having an unsecured receivable. There was a time when that was normal. Now it is not.

Second. Lloyds would have to have GBP on hand to pay over to RBS for my account. Now, while my needs would not trouble the scorers at Lloyds, Lloyds should be looking to ensure it is paid for having GBP on hand, so called liquidity.

Thirdly, instant payment and credit to my account is dependent on the local payments infrastructure. In the UK, the faster payments platform would enable this. Not every country has this. High tech, state-of-the-art technology, which of course needs to be paid for.

The result could be achieved if by chance, just when I want to make that payment, CS had some pounds on hand, but then it runs into laws two and three below. Normally CS would depend on a correspondent, aka Nostro. In the UK to make its GBP payments, such as Llloyds or a peer bank. Even if CS had direct access to the GBP payment systems, via so called self clearing, it has exactly the same challenges that Lloyds faces.

The payments infrastructure in manny countries is likely to be a combination of regulator / central bank oversight of an operating organisation that is owned by the banks. Normally there will be single, monopoly provider, for example CHAPS in UK or SIC in Switzerland. Competition here is not only not needed, but would be counterproductive.

Lessons Learned: Money, or more precisely a connection to the payments systems is the missing ingredient.

The commentators and wise heads who have been lauding the potential of the Blockchain are correct. It is a great invention. The missing link is not another invention, but rather the adaptation of existing infrastructure. What is needed is innovation; connecting the old world of payments to the new world of Blockchain, or to be precise Distribute Ledger Technology.

Without that link, link, Blockchain will be just like sex in high school; everybody will be talking about it, but nobody is really doing it.

Before getting too blinded by the potential second coming of the inventor of CDS, it is worth pausing for thought. Whilst the product was undoubtedly brilliant, the back-office or operational was anything but and the missing infrastructure played no small part in the lack of transparency into who owed what to whom that necessitated TARP and the rescue of AIG in the U.S. as well as massive state bailouts in the UK and Europe. With due apologies to any Classicists reading this, “timeo mercator et dona ferentes”. Beware the trader even when she brings gifts.

More next week on how to bridge between the old world and the new.

Understanding Bitcoin

My own epiphany in matters Bitcoin and distributed ledger technology is the result of three independent sources: I am indebted to Emmanuel Mogenet at Google for his inspiring gift of a Bitcoin, to Richard Brown at IBM for so readily sharing views and educating the latecomer and finally to Reid Hoffman for his seminal article in the May 2015 edition of Wired UK: “Reid Hoffman: Why the block chain matters.”

Previous Posts

Are available on the 3C Advisory website, click here.

Publications

The Bankers’ Plumber’s Handbook

How to do Operations in an Investment Bank, or Not! Includes all the Blog Posts, with the benefit of context and detailed explanations of the issues. True stories about where things go wrong in the world of banking. Available in hard copy only.

Cash & Liquidity Management

An up to date view of the latest issues and how BCBS guidance that comes into force from Jan 1 2015 will affect this area of banking. Kindle and hard copy.

Hard Copy via Create Space: Click here

Amazon UK: Click here

Amazon US: Click Here

Thanks for your support and thanks to the numerous contributors.

Share on: