In the 25 years I have been in banking, one of the major changes is the number of mandatory changes that have to be managed at once and their impact. In the first quarter of 2013, I was discussing this challenge with a potential client, a medium sized Swiss private bank. By their reckoning, their own list of externally mandated projects ran to 160 separate items. Just keeping track of them would be a full-time job.

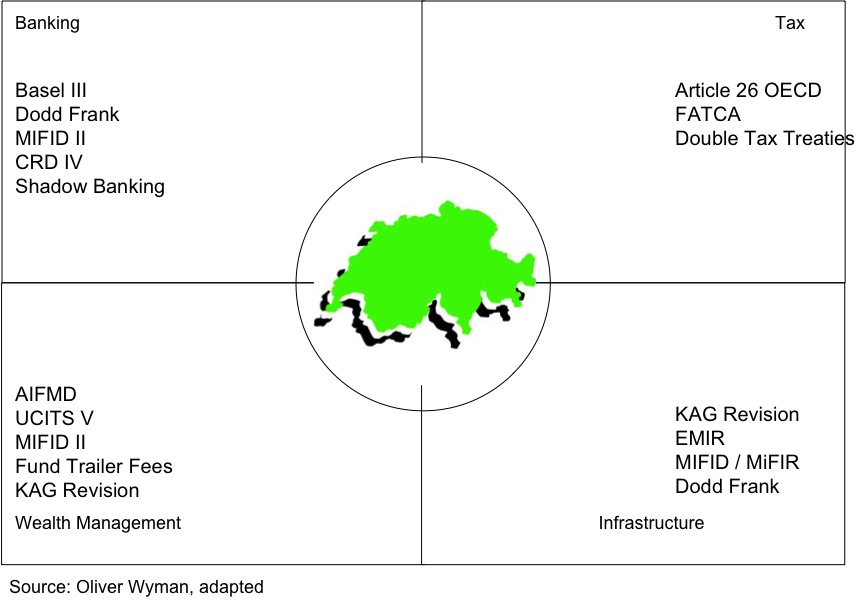

The graphic gives a summary overview of the landscape in early 2013. Albeit a Swiss one, but pretty representative.

On the banking front, Basel III governs the amount of capital that banks need to hold, the risk weightings of their assets and what is considered capital. Dodd Frank has been mentioned in detail above. MIFID II is a European Unioon (EU) directive: Markets in Financial Instrument Directive (MiFID), covering areas such as: transparency, investor protection and EU passporting, MIFID II is the EU response to many issues raised by the financial crisis of 2008 and thereafter[1]. CRD IV is the EU’s set of rules around Basel III; it’s capital requirements directive. Shadow banking is about all of the activities, such as hedge funds, that fall outside the traditional definition of banking. On the tax front, OECD Article 26 is a Model Tax Convention rule from 2012 mandating much wider cooperation between countries on enquiries in relation to tax matters[2]. Double Tax Treaties are constantly evolving, particularly in Switzerland and require close study. On the Wealth Management front: AIFMD, the Alternative Investment Fund Managers Directive[3] is a MIFID for those managers involved with alternative investment vehicles, such as hedge funds. UCITS V is the regulatory work for the more mundane world of mutual funds that are sold to the general public, or as they are formally called in Europe “Undertakings for Collective Investment in Transferable Securities[4]”. Fund trailer fees is all about the commissions on funds that have traditionally been paid by the funds to banks and just as traditionally not passed on to clients. The key word here is transparency; making it very public who is paying or being paid for what. The “KAG Revision” is the Swiss equivalent of this since Switzerland is not in the EU. On the infrastructure front, MIFiR is the regulation that goes with the MIFID directive. A lot of the regulation covers derivatives and CCP’s. Again competition is pushed with limitations on the ties between CCP’s and Exchanges[5], as well as rules o cross-margining or offsetting of similar contracts.

With all this must do stuff on the agenda, it is extremely difficult for any organisation to even make sure that the must do stuff gets done. It is not hard to imagine that many of those efforts will be “best efforts”; just enough to get a tick in the box, maybe with a thought to more robust solutions, but a real politik that means that “just good enough” is all you will be able to do. One senior change manager in a Tier 1 bank told me that for 2013, his budget is 85% mandatory projects to 15% discretionary ones. So, any discretionary projects are going to be very hard to do. They are still worth fighting for.

In my days at Goldman Sachs I would often bemoan some of the US regulations and how I found them a real burden on what we were doing outside of the US. A wise sage, John Frankel, who went on a highly successful career in venture capital with FF Ventures, suggested I need to re-think my view of this: “Regulation is actually good for a place like Goldman Sachs. We have the resources to master it and when we have we can out manoeuvre those who have not been able to master it!” Another way of putting this is: “Go big or go home.” In order to master the increasingly complex demands of the banking worlds, banks have three choices: i) Size. Getting and staying big enough to carry the huge costs across a broad base. In private banking, the perceived wisdom has it that you need at least $100 billion in AuM, assets under management, to effectively carry the costs, ii) Selected Focus. You cannot be all things to all people. In Investment Banking, UBS is cutting back, focussing on those businesses that more directly support its private banking, iii) Sell. Having a small “me too” business will be both too expensive and too risky.

“Too risky” is something that must give pause for thought. Ignoring regulations is not going to work. Earlier in the book, we detailed the case of Bank Wegelin, who were forced to close after being prosecuted by the US government. The cost of being out of line with regulations and laws is no longer a slap on the wrist. It is crippling fines and licences being taken away.

In March 2013 press reports suggested that Britain’s Lloyds Bank was ready to sell its Swiss private banking business. That may or may not have been the case, however with AuM of just $12 billion or so, it is worth thinking of that situation in terms of the choices above for an institution with a business of that size. First off, if another private bank thinks there are 160 must do things that they need to track and they have over 1’000 people and over $80 billion in AuM, how well do you think any outfit, Lloyds or the next guys, are doing with that list of 160? Even knowing the right number is a significant challenge. Option (i) above, to go for size, seems too much of a stretch. Option (ii) focus, might work, but 12 billion is still hugely short of the 100 billion threshold to carry the load of the infrastructure costs.

Lessons Learned: At a minimum, the regulatory changes ought to lead to some consolidation in banking, with some selling and some simply exiting businesses. There will also be some location competition with the new rules restricting some areas of compensation possibly putting traditional centres under pressure.

A personal request: The book of the Blog is in the works. Your support would be appreciated on two fronts:

- Please subscribe, if you don’t already.

- Please share this with a friend or two and ask them to subscribe too.

If the comments are wide of the mark and not offering anything of use, please comment or make contact directly via E-Mail.

[1] For more detail, see: http://www.deloitte.com/view/en_LU/lu/market-challenges/mifidii/index.htm#.UU8yOb-Yo7Q

[2] For more detail, see: http://www.oecd.org/newsroom/taxoecdupdatesoecdmodeltaxconventiontoextendinformationrequeststogroups.htm

[3] For more detail, see: http://ec.europa.eu/internal_market/investment/alternative_investments/index_en.htm

[4] For more detail, see: http://europa.eu/rapid/press-release_MEMO-12-515_en.htm

Share on: