With new rules coming into effect on Jan 1 2015, this is the tenth in a series of posts on how banks and FI’s might adapt. And, the book on matters liquidity, as well as general one on Operations is now available.

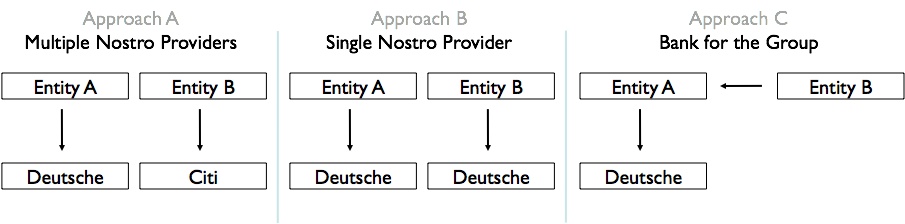

There are three standard models for the Network Management (NetMan) set up:

Approach A – Multiple Nostro Providers: this is the most common approach, with entities within a group not using the same provider. Mostly this is down to a lack of co-ordination and an absence of any central control, quite often sprinkled with a soupçon of ignorance.

Approach B – Single Nostro Provider: in this format, a decision is made as to who the Nostro provider is in a currency and all group entities bank there.

Approach C – Bank for the Group: this is the idea that UBS followed and I recounted in the prior post. In the post-Lehman world, this set-up may invite regulatory scrutiny. In the Lehman set-up, there was a degree of this “bank for the bank” in the structure. The bookkeeping was not 100% robust, and some payments got rather stuck in the bankruptcy.

In thinking about intraday credit taken, it is important to understand that this is not a “net group wide” number; debit and credit balances cannot be universally netted. Only a limited degree of netting is allowed to branches in the same jurisdiction; however, netting bank and broker-dealer entities is not permitted. This is one more reason to use Approach C, the “Bank for the Group”.

In the previous post, we discussed one of the key controls that the NetMan team ought to exercise, mainly having the smallest possible number of accounts or depots and having a global NetMan organisation with a single set of controls around account opening. That is really the basic step with a sound rationale.

Once an entity is part of a larger group, there is a more advanced part to control, namely, how the group as a whole operates. At the group level, banks tend to be quite complex, and multiple legal entities are the norm, as is a high volume of inter-company transactions and loan activity. If the entities in a group were wholly independent and had nothing to do with each other, then having multiple Nostro providers might be fine. This is approach A . For simplicity here, the reference is to Nostros; however, the same holds true for depots or custodians.

It is important to understand how high the levels of inter-company transactions are. My experience has been that this is underestimated. There are several reasons that you need to be sensitive to this:

Credit Lines

In approach A above, if Entity A has to make a payment to Entity B, it may need to rely on credit from Deutsche. That may conflict with a payment that Entity A has to make to a client. Deutsche, like any Nostro, will treat all payments where “money is going out the door” as needing credit.

In approach B, any movements between Entities A and B are internal within Deutsche. They do not require credit. They will be settled by what is called a “book transfer”. This leaves the maximum credit available for client and counterpart payments.

Cost

As a rule, both Nostros and depots will charge less for book transfers than for external transactions.

Liquidity Buffers

There are two impacts here, firstly, on the entities as credit takers, and secondly, on the Nostros as credit givers.

The latest guidance on intraday liquidity planning and reserves requires both credit takers and credit givers to have reserves to cover their exposures. In very simple terms, it effectively requires credit takers and credit givers to have insurance against the lines they use or give.

This is rather like house contents insurance. The more you use or give, the bigger the absolute size of the liquidity buffer, which is the insurance policy. A rule of thumb is that this is between a floor of 10% and a cap of 20% of the exposure. The BCBS guidance looks at the peak intraday overdraft. So if across many Nostros you are “taking” peak credit of USD 10 billion, they will expect to you to have at least 10%, $1 billion, in a reserve. The cost of carry for this will vary between 100 and 150 bps. “Cost of carry” means the cost to borrow the funds, less what you can earn on the bonds you invest in by repo’ing them out.

So from a credit taker’s perspective, there is potential double jeopardy here. They have to insure for what they take from the Nostros, and the Nostros have to insure what they give, which is a cost they will look to pass on.

There is a credit-related argument that suggests that a group might want to maximise the credit available by following Approach A. This is a plausible argument for A, but one that is more than countered by the case for Approach B, based on the issues highlighted above. Simply put, the absolute minimal group standard or “philosophy” must be to have all entities use the same provider for the same service in the same market. It may be the case that securities settlement is with a different provider than the payments business. That is acceptable as long as all securities settlement is with the one provider, and all payments or Nostro accounts are with one provider.

There is an opportunity to optimise further by using a “bank for the group”; this is Approach C. If Entity A in your group is a provider of Nostro or depot services, it could service the other group companies. The net result would be that there would only be one account in the real world, which would minimise costs. For Approach C to work, Entity A has to be able to deal with the processing and accounting for the other entities. Entity A does not have to be a self-clearer, so it could, as in the example, use a service from Deutsche Bank. Entity A, though, needs to be able to provide a full set of services to Entity B and any other group companies. In the Nostro world, this is the ability to process and send SWIFT messages. For example, Entity B will want to receive a bank statement in SWIFT MT950 format to feed into its reconciliations engine. I have seen this work; for example, the two major Swiss banks, CS and UBS, have all the capabilities, as they are themselves providers of Nostro services to other banks and institutions.

It can fail too. Unwinding the Lehman empire after its collapse was complicated by the fact that Lehman Brothers International (LBI) acted as Nostro and custodian for some of the smaller group entities. However, it was doing this without the full set of services and functionality that would be required. So monies belonging to some of the smaller subsidiaries were entangled in the bankruptcy of LBI.

Bank groups are indeed generally complex, with many legal entities. In the case of Lehman, there were some 2,000 companies. Aside from the Dodd-Frank regulations and their European pendant, EMIR, another outcome from the Lehman collapse has been that the regulators have pushed banks to have something called a “living will”, essentially a guidebook that would assist an administrator in a bankruptcy event. In the UK, the formal title for this is Recovery & Resolution Planning. There is particular emphasis here on documenting inter-company relationships, both in terms of trades and in terms of treasury loan activity, and on having plans for how to operate the entity in a bankruptcy event. This would not exclude one legal entity providing services for other group companies; after all, you could not imagine that Citibank would have its broker-dealer use JP Morgan for its USD Nostro. The key point is that if you were to do this, there would be more scrutiny to ensure that it was being done accurately and properly.

An example of the kind of issue you might face is “unsecured receivables”. If, in Approach C, Entity B has a long cash balance of, say, $100 million with Entity A, in B’s books that is an “unsecured receivable”. Depending on the jurisdiction that B is in and its own capital, there will be large exposure limits on what it may have open with group companies as a whole. These will likely vary between secured and unsecured, the latter having higher exposure limits, as the risk is greater. Now, as long as there are good processes in place, Entity B can always avoid having an unsecured receivable with A, for example by entering into a repo trade or making a loan to an entity it can loan money to. But the process has to work without fault.

If you have the infrastructure to properly support Approach C, this can be a good thing. If you do not want to go that far, then there is a variation for payments in Approach C that you should consider. In the early part of this section, the case was made for having as few Nostros or depots as possible. Splitting up securities activity across multiple depots is not practical; you are bound to end up with the shares or bonds in the wrong place. However, payments are easier to split out. The variation to Approach C would say that you use a “bank for the group” for all inter-company payments, so all group entities operate a Nostro with Entity A in every working currency. Any payment to another group company is then routed via Entity A. This will reduce costs and will reduce the use of credit lines.

Given that inter-company transactions are often a sizable minority of the activity, internalising that activity can make a substantial contribution to keeping the increasing cost down of paying for the liquidity buffer costs.

Lessons Learned: NetMan is something that has to be central, active and absolute. There is no room for “agreeing to disagree” or as it used to be titled at IBM: “non-concur”. The folk in charge have to have a view and need to enforce it.

A personal request: Finally. I have ventured into self-publishing.

And, the not so creatively titled, but practical guide: “Cash & Liquidity Management: Mastering the Challenges of New Regulations and a Changing Marketplace” is now available in print and on Kindle. All the bits form the Blog are there, together with a lot of detail on current challenges. Many of those challenges will take effect on Jan 1 2015. Time to be well informed!

UK: For the print version and Kindle users: Click Here

US: For the print version and Kindle users: Click Here

Hot on its heels is a book on wider operational matters: The Bankers’ Plumber’s Handbook. Coming soon.

Thanks for your support and thanks to the numerous contributors.

Share on: